Residential & Commercials Loans

We know that each customer has specific needs, so we strive to meet those specific needs with a wide array of products, investment tools, mortgages and best of all quality service and individual attention.

Today's technology is providing a more productive environment to work in. For example, through our website you can submit a complete on-line, secure loan application or pre-qualify for a home loan. You may also evaluate your different financing options by using our interactive calculators and going over various mortgage scenarios.

Bring us a Loan Estimate from another lender, and we’ll beat it whenever possible. If we can’t beat it—and you provide proof you closed with that lender—we’ll pay you $1,000.

Terms and verification requirements apply. Click here for full details.

A conventional loan is a type of loan that is not insured by the government. Conventional loans offer more flexibility and fewer restrictions for borrowers, especially those borrowers with good credit and steady income.

FHA home loans are mortgages which are insured by the Federal Housing Administration (FHA), allowing borrowers to get low mortgage rates with a minimal down payment.

VA loans are mortgages guaranteed by the Department of Veteran Affairs. These loans offer military veterans exceptional benefits, including low interest rates and no ...

A jumbo loan is a mortgage used to finance properties that are too expensive for a conventional conforming loan. The maximum amount for a conforming loan is $766,550 in...

A USDA loan is a type of mortgage that is backed by the U.S. Department of Agriculture and is designed to help eligible borrowers buy homes in approved rural and some suburban areas. USDA loans typically offer benefits like no down payment, competitive interest rates, and reduced mortgage insurance costs for qualifying low‑ to moderate‑income borrowers.

A DSCR loan is an investment mortgage that qualifies mainly on the property’s rental income, not your personal income. The key factor is whether rent covers the mortgage payment and expenses.

A construction loan is a short‑term loan that covers the cost to build or majorly renovate a home, with funds released in draws as each stage of construction is completed. Lenders typically require detailed plans, budgets, and inspections, and once the home is finished, many borrowers either refinance into a regular mortgage or convert the loan to permanent financing.

An SBA loan is a business loan issued by a bank or lender but partially guaranteed by the U.S. Small Business Administration, which helps reduce the lender’s risk. These loans are designed for small businesses and often feature longer terms and more favorable rates than many conventional business loans.

A fix & flip loan is a short‑term financing option for real estate investors who want to purchase, renovate, and quickly resell a property for profit, often within 6–18 months. These loans are typically based more on the property’s after‑repair value (ARV) than the borrower’s income, and can cover both the purchase price and rehab costs, usually at higher interest rates in exchange for speed and flexibility.

A fixer‑upper loan is a type of mortgage that lets you buy a home and finance repairs or renovations together, instead of taking out a separate rehab loan or paying cash for the work. These loans are designed for properties that need updates, allowing you to roll both the purchase price and approved renovation costs into one loan with a single monthly payment.

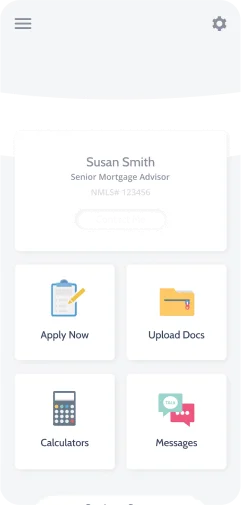

The Loanzify App guides you through your mortgage financing and connects you directly to your loan officer and realtor.

Tools to get you informed and started on your mortgage journey.